Over the weekend, Kevin Drum joined those who have had the “seriously? This is all we are going to do in response to the largest financial crisis in 80 years!?” freak-out moment. (I’ve had several. Trust me, I’ve had several.)

The realization, and I’ve reflected on this a lot, is that we are rebuilding the 2007 financial sector with some additional legal powers for regulators to exercise in the middle-of-the-next financial crisis. I encourage Kevin, when he’s in a safe place, to reflect on it from the point of view of the biggest players, if they had survived.

Over the next few years your major competitors in the regionals are going to be crushed by the wave of CRL losses, while the government is never going to touch your second-lien exposures, furthering that concentration. We’ll see what happens with derivatives, and I am rooting for the Lincoln Bill to survive. Maybe we’ll actually get involved with suing the banks for fraud. There’s still some hope out there. But it’s very likely you’ll look at it all and think things are pretty much ok.

A few additional things:

1) Break up the largest banks in addition to the current bill. Forget feasibility. Once you stand back and realize that structural change is necessary in addition to the prudential regulation stuff, the whole things feels better. It’ll probably lose – but what a good idea to lose on.

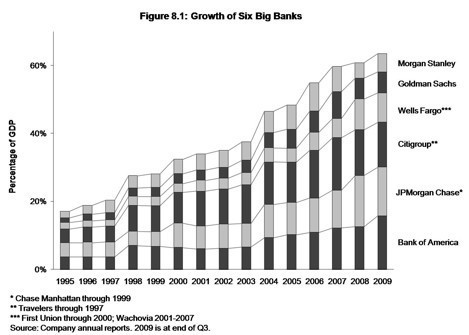

Because it is right. The concentration is from non-existent anti-trust law over the past few decades. There’s no advantage to them that anyone can quantify.

2) The new status quo will be even worse. Listen for allusions to the canadian banking sector. It’s a poor analogy, first off. But it also involve an even higher level of, as Steve Randy Waldman horrified me a little over a year ago by pointing out, the largest parts of the financial sector shaking hands with the government in a way that should scare us. What percent of the corporate profits that go to finance look like in 2014?

3) In some ways it’s a very exciting time to be thinking about financial reform. I’m thinking about Dean Baker’s financial transaction tax, Zephyr Teachout’s new financial anti-trust law, Jane D’Arista new financial regulatory infrastructure, Waldman-ian delinking of FDIC insurance, and a ton of other things. So is the Right, thinking through CDS as a resolution mechanism. We could do all this now, especially a financial transaction tax or a really serious tax on liabilities. But most of this will have to wait until the next financial crisis to come under serious discussion again, but hopefully we’ll be ready this next time, and sadly the doom loop might amplify to the point where we have to take more serious action. I wish we could sail this reform into the sunset, but most of the major players say that a financial crisis every 6-10 years is the new normal.

And our last financial crisis was already 2 years ago.

Heard Mike on Marketplace this morning. Right on.

In addition to other measures, I wonder: why not (a) institute the Volcker Rule forbidding regulated banks from trading on their own accounts, and then (b) require that any firm that does trade on its own account be structured as a partnership (or: any other form that lacks limited liability, and lets creditors come after partners’ assets.) I think it would concentrate the mind.

Hilzoy makes some sense, especially around “concentrating the mind” ie market discipline from creditors. The Volcker rule alone will not regulate the shadow banking system, but the “partnership” would help bring some discipline to them, along with prudential reg

I think opponents of these policies need stronger arguments and more effective organization, drawing together the broad spectrum of Americans and indeed world citizens who are adversely effected by these policies.

To do this:

1. The enormous cost of these policies must be demonstrated and emphasized in simple and clear terms. The problem needs to be phrased in terms of people’s pocketbooks, their take home pay, their savings and retirement funds, and the profits of the many small and medium sized businesses suffering from these policies. For example,

http://www.cepr.net/index.php/publications/reports/too-big-to-fail-subsidy/

There have been efforts in this direction such as Joseph Stiglitz’s recent book Free Fall, some of Simon Johnson’s articles, and so forth, but more, more effective and more concise statements are needed. The murky system of implicit and explicit government guarantees, shadow bailouts using the Federal Reserve, Treasury, Fannie Mae, Freddie Mac, and so forth needs to be effectively exposed. This is a shell game, like three card Monty on a trillion dollar scale, designed to confuse and distract most Americans.

2. The use of terms like “investment”, “growth”, “innovation”, and “research and development” to promote and defend these policies needs to be aggressively confronted and debunked. It needs to be made clear that the trillions of dollars spent on housing in the 00’s and goofy telecom and Internet schemes in the 90’s represents trillions of dollars not spent on critical human needs such as energy production, more efficient energy systems, transportation, and so forth. We see the consequences of this in rising energy prices and a declining standard of living. Yet another bubble, whether involving investments in China or blinking gadgets here at home, would represent further disastrous diversion of trillions of dollars from productive activities.

3. The framing of the problem as one of “deregulation” versus “regulation”, the “free market” versus the “government” needs to be rebutted and avoided. Quite clearly, these are policies of huge government subsidies to a few giant politically connected banks. The fact that these banks have stockholders and the executives are not civil servants (they are in fact paid far more than civil servants and subject to less strict rules) does not mean they are not intimately connected with the government. It is certainly true the policies have been and continue to be promoted with labels such as “free market”, “deregulation”, “private sector” and so forth, but the reality is otherwise. Many businesses and people outside of a small and shrinking charmed circle are suffering from these policies, but are misled by the “free market” rhetoric. The implicit and explicit claims by the banks to represent the “free market” or “private sector” should be aggressively challenged and debunked; they are almost laughably absurd at this point.

4. The long standing tactic of blaming the failure of policies labeled as “free market” and similar terms (emphasis on labeled), with the failure then used to promote further policies labeled as “free market” or “deregulation”, on the government should be recognized and aggressively countered. Blaming the government for fiascos that follow policies labeled as “free market” is not unusual. It happened after the Savings and Loan fiasco of the 1980’s, the Internet bubble, the Great Depression, the California electricity market “deregulation” fiasco of 2000, and a number of other cases. Rather, this long history of “crying wolf” should be pointed out simply and clearly, that the purported “free market” policies are frequently selective deregulation combined with increases in government subsidies for politically connected firms, and once again that the aggresive use of labels such as “free market” does not mean the policy actually is “free market”. Certainly not in the case of the current Too Big to Fail policies nor the sharp increase in FSLIC guarantees during the Savings and Loan “deregulation” of the 1980’s.

Drawing a clear distinction between the present policies fraudulently promoted as “free market” or “deregulation” and actual “free market” or “deregulation” policies will enable opponents of these policies to reach out to private citizens, businesses, and organization across the political spectrum, all of whom are suffering greatly from these policies.

Sincerely,

John

So why didn’t Canada suffer any bank crises during the Great Depression? They didn’t even have a central bank until 1935, so it can’t be lender of last resort powers.

Breaking up the big banks and preserving positive aspects of the Canadian system are not mutually exclusive. One major advantage to Canada’s banking system is about branches, not about size per se. Why not split the banks geographically, so Chase (1) and Chase(2) each get half the California branches, half of the Texas branches, half the Illinois branches, etc. by region and state.

One of the major points of branch banking is to spread risk, as most housing loans are local. It’s no coincidence that IndyMac and Washington Mutual were very active in bubble areas like California.

It’s interesting and important how much of these problems wouldn’t exist, or would be far less, if we had really strong public campaign finance and corporate contribution limits.

(Tremendously increased public campaign finance could be done by the President and Congress; strong contribution limits may require a replacement of one of the Republican Supreme Court justices or an amendment, although some creative legislation could be effective in substantially limiting the power of corporate spending)

A lot of times the most powerful way to tackle a problem is indirectly (or a combination of directly and indirectly). Some of the best things we could do to tackle great issues like finance reform and global warming are indirect, politically structural, things like abolishing the filibuster, tremendously increasing public campaign finance, and ending or greatly limiting corporate campaign spending, or at least making it a lot more transparent and difficult.

Without addressing energy consumption in particular – and the bad habit of living beyond our means in every sense – the next deleveraging leg is already upon us. This is the result of dollar hardening around the high – but pretty, pretty please no higher – price of crude.

A dollar pegged to crude is the last thing the finance universe can deal with and the effects are being manifest in the Eurozone and in China. All bubbles are wealth hedges against rising input costs – including but not limited to (real) credit and energy costs. In the end the hedges fail with the stumbling block being deflationary currency ‘worth’.

Unfortunately, resource constraints and the effects of depletion are not to be regulated around. Because of politics and inertia nothing will be attempted to address core issues until after the next crashing event is well underway. By then, it will be too late and resource conservation will be effected upon (the survivors) by circumstance.

The overhang of non- collectible debt represents the potential energy factor available to smash the current, weakened finance infrastructure. Deleveraging can be an outcome of hard money on one hand or the rising tide of ‘repudiationism’, where loan obligations become options for suckers and trust vanishes. Repudiationism is a manifestation of currency preference over credit, although repudiation coupled with vacation spending is somewhat bizarre.

One of the characteristics of this crisis is what I call the, “Nobody listens to me I’m an idiot” effect. Read Stiglitz, James Grant, D’Arista, Prechter, Schiff, Minsky, Henry Kaufmann – and particularly M. King Hubbert – the outlines of the current mess were relatively clear decades ago.

But … nobody paid attention. Why start now?

Pingback: ginandtacos.com » Blog Archive » HERESTHETICS