Late to a couple of discussions. One is this slacktivist on HR using people’s credit scores as a filter on their jobs:

Some 14.6 million Americans are out of work. Nearly 7 million of those are long-term unemployed — people who haven’t been able to find a job in more than half a year. Those millions of Americans, as a direct consequence of being out of work, have lower credit scores. Those millions of Americans, as a direct consequence of looking for work, have lower credit scores. The credit agencies say that therefore the unemployed ought to remain unemployed.

….The use of credit checks in employment decisions should be banned. It is a form of discrimination against the poor — the codification and enforcement of class barriers. It is therefore a form of discrimination against those groups more likely to be poor and therefore a violation of the 14th Amendment. So it ought to be illegal already.

It’s also cruel, costly, bad for business and bad for America. Outlaw it. Make the practice — both the use of such scores and the provision or marketing of such scores for that use — punishable by fines and imprisonment. Make the punishment large enough that employees practicing this form of discrimination know that it will involve serious repercussions — harm to their firm’s “assets, reputation and security.

Kevin Drum, Matt Yglesias and Matthew Rognlie (whose blog I just found and is worth following) have more.

Two things:

1) Let’s pretend I moved into a really crappy apartment in Brooklyn. Impossible to imagine, but let’s try. And while it looked fine on the walkthrough, it turned out to have all kinds of problems. Worse, the landlord doesn’t return my calls, doesn’t do the upkeep he promised, etc.

What’s my option? To threaten to not pay my rent and/or break my lease. That’s my real credible threat. He can hit my credit score if I don’t pay in return. I understand that I would then have a harder time finding an apartment, securing lines of credit, etc. but that may be worth it to keep my landlord in check. To the extent that a bad landlord will upkeep my apartment it is because if I don’t he or she knows I can take a credit score hit and walk away.

So as a result of a bad role of the life dice, I could end up with a bad credit score simply as a result of exercising basic contractual rights to keep myself from being screwed. Now if me protecting myself from being screwed could add weeks or months to duration of unemployment…suddenly that landlord can show up a few days later in fixing my broken shower.

Credit scoring isn’t some sort of impartial measurement, like taking my height or weight. It’s part of a game that I play with creditors; it’s a game that usually works fine until it doesn’t. When it doesn’t, having my ability to search for jobs imperiled cuts off my ability to negotiate for myself. Isn’t it worthwhile to keep these dimensions of ourselves separate?

I’ve also heard a lot about it being difficult to challenge FICO scores. I’m not sure if this is true or not, it’s always something I’ve wanted to investigate, but I’ve heard that. To the extent that it is difficult to challenge it is hardest for those with poor access to legal services or those who are disconnected from the formal credit economy.

It’s the Aggregate Demand!

2) In the short term, this is a sideshow. Slacktivist argues this is one of the reasons unemployment is so high right now and the recovery is slow. I doubt that. The real reason HR people can behave as mini-tyrants?

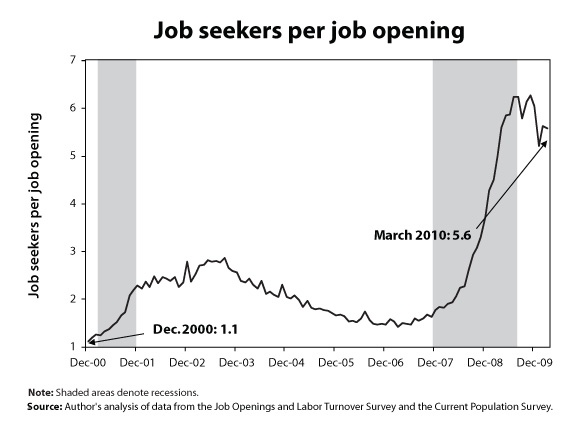

Scott Winship has a chart showing unemployed per job opening:

EPI follows this as well:

There’s simply a lot of people looking for jobs. At the margins, it’s worth it for HR to spend extra time searching for employees because there’s no rush to produce goods or services. Meanwhile there’s a complete lack of aggregate demand. Companies are sitting on cash instead of using it to build and hire. If inflation spurred investment, if the government could stoke aggregate demand, then suddenly employees would have more bargaining power and HR reps would get yelled at if jobs weren’t filled because new work needs to get done, and this would likely go away as a problem.

I’m curious as to the long-term effects of 10% unemployment. Could we see a new cultural or legal equilibrium form that gave even more power to employers over employees if we slowly drag ourselves out of this recession Japan style?

UPDATE: Whoops. I don’t think that renter’s example is relevant at all. Oh well. It would be true of other consumer debts.

But credit reports give all your accounts and balances and payment status. I wonder if that would be a good measure of how liquidity constrained a person is, and as such how quickly they’d be willing to bargain for a job. If someone is about to go broke, he’ll take a job with fewer benefits. etc. If an employer know that, but the applicant doesn’t know how quickly the firm needs the job filled, there’s an asymmetry there. That actually strikes me as far more insidious.

As a Canadian, I was incredulous that this practice even existed until I saw the request for a credit check on an application form for an American company. I didn’t fill out that application.

It occurs to me, however, that an HR person’s job is effectively to come up with (legal) reasons to slash your résumé from the pile. A credit check is a relatively inexpensive way to do that. Not unlike a police intervention, “anything you say can and will be used against you”, so submitting to a credit check reduces to arming the organization with not only the means to discard you, but potentially the means to low-ball you if they do decide to give you the job (reasoning: if you have a low credit score you might be eager to take any deal to pay off your obligations).

Of course, denying the credit check in the very least puts you in direct competition with people who permit it, and at most summarily takes you out of the running. It’s the kind of norm that demands enough people to say “that’s none of your damn business” to change, which in a high-unemployment market is unlikely. Banning the practice just squashes the problem out in funny ways, like it does for other modes of discrimination.

I wonder, though, if we started treating the labour contract as a peer relationship rather than a paternalistic one, we could circumvent a lot of the demeaning activity that goes on in HR land. With decision-makers making themselves more accessible (e.g. LinkedIn, Twitter, Facebook) it is much easier to contact them directly than it has been in the past. This is not to say that there won’t be significant adjustment on the parts of both job-seekers and employers, and that it won’t spend a significant period in the higher-profile sectors, but these kinds of changes have a funny way of democratizing themselves. It’s probably better in the long run to treat employment like a voluntary, reciprocal, ultimately social relationship, not like a bond of indenture.

As a footnote, if anyone can’t wait for the scourge of pre-employment credit checks and other incursions to end, one can always move to Canada.

Whoops. I don’t think that renter’s example is relevant at all. Oh well. It would be true of other consumer debts.

But credit reports give all your accounts and balances and payment status. I wonder if that would be a good measure of how liquidity constrained a person is, and as such how quickly they’d be willing to bargain for a job. If someone is about to go broke, he’ll take a job with fewer benefits. etc.

Thanks Dorian,

“One can always move to Canada” is in the background of many people’s mind.

Glad you’re blogging on this, Mike. (We met briefly at Zephyr Teachout’s bank size conference.) The “exercise of rights” example is great, and, sad to say, some free marketeers think that’s why the credit scoring is just peachy: it deters people from taking advantage of the oh-so-bothersome legal system.

I’ve blogged a bit on the racial disparities here:

http://balkin.blogspot.com/2010/07/credit-scoring-faces-at-bottom-of-bell.html

The bottom line is that we really, really need to know more about how the scoring is done.

Let me try to present the argument for using credit scores in employment decisions. I’m not sure I buy it, but it is a decent argument:

1. You find good (and bad) credit scores all across the income ladder. One could even argue that the worst effect of credit scores on poor people is that they just don’t have them, often not being in the credit economy. The Boston Fed did a study along this line about 10-15 years ago, in connection with CRA. Some banks subsequently developed credit measures linked to bill-paying, rather than paying borrowed-money debts. Maybe FICO followed–I’m not sure. But even if so, there is no information if you’re solely in the informal economy. It might be worth noting that insurance regulators, in many states, do not allow an insurer to draw any inferences from a lack of credit scores.

2. If properly used, credit scoring can be useful in employment contexts. A crappy credit score can mean anything: unemployment, medical problems, divorce, a gambling jones. Properly used, a credit score is an invitation to further questions, not the basis for a decision. I sure wouldn’t want to hire a person with a gambling habit in any position of trust. (Would you?) We have something like this with the Americans with Disabilities Act–you can’t legally use a perceived disability in a preliminary decision to hire, but can use it later, to check whether the person can actually do the job.

Of course, both of these points have their limits. Credit scores might (or might not) be unfair to groups, but they sure can be unfair to individuals. And, in a labor market like this one, employers are likely to use credit scores as a primary screen. A prohibition of credit scoring in employment decisions is rational. But so is regulated use.

In the case of the rental dispute, non-payment over a dispute is something that could be reported to a credit agency — although this would likely happen only in the case where you were sued for the non-payment. Most likely, the money would need to be put in escrow until the dispute was resolved. Of course, knowing these kind of options probably requires some understanding of local landlord and tenant laws — an area where education and income matter. Simply deciding not to pay might put you in jeopardy even if you had a legitimate claim.

I agree with the larger point though about how credit scores are usually irrelevant for most kind of jobs; the evidence linking credit scores to employment performance is dubious; and the practice should be banned in all but the most narrow set of circumstances (e.g. jobs requiring security clearances, or jobs involving finance).

Join the Fight and Make the BS Come to an End!!!!!!

In survey after survey, including a recent MSNBC survey, more than 90 percent of Americans say that workplace discrimination based upon someone’s personal credit report is wrong and should be illegal. ZERO statistical evidence exists to tie bad credit reports to fraud! It’s already illegal in 3 states and HR3149: The Equal Employment for All Act would make it illegal in every state, but most Americans don’t even know the legislation exists. Please support the overwhelming will of the people and the rights of highly qualified American workers to compete on a level playing field during this horrible economic disaster. Join our FB PAG at: http://groups.to/h.r.3149 or shoot us an e-mail at hr3149@hotmail.com with”sign me up” in the subject line.