Numbered lists! Paul Krugman posts six reforms ideas, which along with the four goals list of Ezra Klein are the two best numbered lists of things to consider in this financial reform debate I’ve seen lately.

Ryan Avent was interested in this argument:

Next, Mr Krugman had another interesting thought that I’ve been musing on for a couple of days. He said he’d been having the uncomfortable feeling that the crisis-free years of the postwar period had little to do with any particular financial regulation and a lot to do with the franchise value of banks. The banking sector, at that time, was highly uncompetitive. The lack of competition made bankers fat, happy, and risk averse. When the banking sector was deregulated, banks had to work for their money. This led to some improvements in customer experience, but it also made bankers more aggressive in their pursuit of new profits (particularly as public ownership of large financial companies became more common). This increased the involvement of big banks in dangerous financial activities, which led to growth in systemic risks.

And Yglesias has more, including a good Gary Gorton article.

I’m still thinking through a lot of this story of the financial industry in the past 30 years, the pieces of evidence for it and the implications it would have. I want to make this story of 1980-2010 a little bit more complicated by introducing two stylized facts that aren’t easy to reconcile: (1) though competition increased in the financial sector post-boring banking so did financial sector profits and (2) the concentration of the financial sector increased in the post-boring banking era.

Graphs! Which leads to a bigger question I’ve been thinking of lately: In what ways did 1980-2000 deregulations change the financial sector? This goes to the franchise value question. First off, it’s true that there are a lot of new players to the financial space post-1980:

But let’s look at some graphs comparing finance to other deregulated sectors from the early 1980s. From Doug Henwood, here are wages in the trucking industry following early 1980s deregulation, when the franchise started to collapse:

![]()

And from the Federal Reserve Bank of San Francisco, a study of airline deregulation. They concludes “while profits have fluctuated a great deal, the industry in the U.S. has been characterized by steady growth, falling prices, and moderate concentration, suggesting a positive impact of deregulation”, this graph:

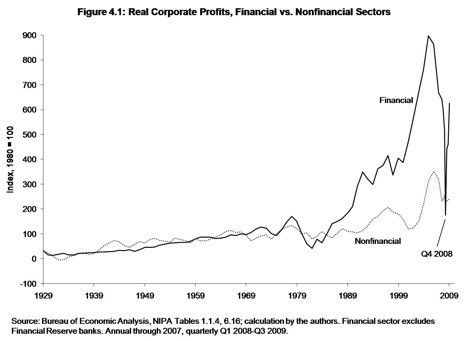

I was actually going to write James Kwak last week and tell him to get his most important graphs from 13 Bankers online for the upcoming financial reform talks, but he’s gone and done that. From 13 Bankers, profits and compensation:

Notice that the protected profits and compensation of the pre-1980 era pale in comparison to the post-1980, and notably post-2000 era. (Everyone brings up how little the money in Liar’s Poker seems to people on Wall Street today and if you re-watch the Oliver Stone movie Wall Street today, the scandals and dollar sums also seem like chump change). So if the financial industry, broadly speaking, was offered a chance to go back to the protected pre-deregulated industry of 1976, I don’t see them jumping at the chance like perhaps trucking or airline industries might. The money makers here are high-yield debt, securitization, arbitrage trading, derivatives and (most importantly) the move of financial intermediation from banks into the capital markets. We could cartelize these activities, and arguably derivatives is already this way among the major market dealers.

Now we could create shadow banking licenses to re-create a cartel, but we currently have a much more concentrated banking sector than we’ve had pre-1980s in the boring period:

I’d also like to throw a link to this paper by James Crotty: “If Financial Market Competition is so Intense, Why are Financial Firm Profits so High?”, which finds the reasons “are: rapid growth in the demand for financial products and services in the past quarter century; rising concentration in most major financial industries that makes what Schumpeter called “corespective” competition and the exercise of market power possible (thus raising the possibility that competition is not universally as intense as Volcker assumed); increased risk-taking among all the major financial market actors that has raised average profit rates; and rapid financial innovation in over-the-counter derivatives that allows giant banks to create and trade complex products with high profit margins.”

I’m still thinking all this through, and these are some of the problems I’m trying to figure out.

I’m not much impressed with the discussion in the US. As Peston said:

http://www.bbc.co.uk/blogs/thereporters/robertpeston/2010/04/bank_reform_the_nutters_in_the.html

“Here’s what’s striking.

First that Turner and King/Haldane are some way apart (King has been very sceptical about the notion of taxing transactions to shrink markets).

But arguably more important is that the Bank of England and the Financial Services Authority are very much the outriders in terms of global thinking about all of this: they are massively more radical than their peers in other financial centres.

And they’re also much more radical than the elected leaders of any rich developed economy.

What you might deduce is that King, Haldane and Turner have somehow acquired immunity from a dangerous prevailing liberal-market ideology that is actively promoted by the banks and bankers who profit from it (this characterisation is not that of some Marxist extremist by the way, but is the FSA chairman’s), but that politicians are yet to acquire that immunity (which some would say is to do with the traffic in jobs between banking and politics, especially in the US).”

what about average compensation per total transactions? or size of the money in the system?

also, what share of world financial transactions appear in the US? If the 1980 – present is a time period of increasing globalization of capital markets, than if the US has more of the world share of transactions, shouldn’t we have more of the spread (and thus income)?

Here’s the way I’m thinking about it:

Pre-80’s, interstate banking was illegal. This resulted in many banking ‘fiefdoms’, uncompetitive markets with few options, but relatively smaller banks.

When regulations restricting interstate banking were relaxed, there was more competition, but also consolidation, leading to a few national mega-banks dominating market share.

So I suppose I’m thinking of pre-80’s banking as feudalism, and the current system as oligarchy. Which is better? Neither are too appealing, but throughout history there do seem to be more examples of feudal systems persisting. Oligarchies seem to eat their own tails.

Hi Mike,

Can you compare the amount of total outsize profits from the post 1980 banking sector to the size of the crater they’ve created in this crisis? I don’t have the data to compare their intake over the last 30 years vs. the total value of all subsidies and bail-outs we’ve had to put in since things went south. (A fair accounting would have to include not only unpaid loans, losses, and equity, but the “good will” we get when packages are offered at below market rates.)

If we are going to say the industry is making more money since deregulation, we should look at the whole cycle. And if that profitability is only maintained by utilizing a huge externality (e.g. they take risk, go bust, we bail them out) then perhaps at least some part of outsized post-1980 profits come from one-way capitalism.

*cheers*

Pingback: FT Alphaville » Further reading

Mike, that Crotty paper is terrific (thanks). It led me to Dallery’s “Post-Keynesian Theories of the Firm under Financialization.” [pdf] There’s a lot of good stuff in it — conflict between labor, management, and capital; the demise of the Galbraithian firm; shareholder demand for profits vs free cash flow; and why financialization means slower growth. I’m not sure if I believe it but at least it’s readable.

As for the oversized financial sector profits, have those been all wiped out now (excluding bailouts)? Maybe Wall St really just a bunch of dummies betting it all on black, but each spin takes so many years that nobody can see what the real game is.

On “If Financial Market Competition is so Intense, Why are Financial Firm Profits so High…” there are quite a lot of good potential reasons for higher margins ie weak competition, high demand, but there’s also operating leverage as a driver of consolidation.

There’s just very high operating leverage in banking. In asset management for example, there’s very little incremental costs to managing more money. Think about an asset manager running $1bn versus $1.5bn AUM–he’s definitely not working 50% harder, nor are they hiring 50% more people.

Similarly, in investment banking, once you get a securitization factory going, have the legal infrastructure, processes and sales/traders in place, there’s a lot of operating leverage. Whether you do a $1bn deal or a $10bn deal, it’s about the same amount of work outside of marketing to more investors (a few more phone calls…)

On the other side of this equation, think about the pricing structure: it’s usually a % of the deal/AUM–that’s the true cream in the business.

Now, you can argue that pricing is a function of weak competition, but I’m not sure I buy it fully. Look at the hedge funds, there are literally thousands of them fighting for funding but through the worst recession, funding environment, horrible HF startup environment, pricing structure hasn’t changed. 2/20 is the old and new black for fees/incentives. That has really puzzled me but I think a lot of the sources of funding, pension funds etc just don’t care about the fees given the potential upside is that much bigger (20% returns! 30%!)

So here’s another possible reason for high margins by banks: their customers (not the retail ones but the companies/institutional funds) just don’t care enough. Board of directors don’t care about negotiating banking fees down (fiduciary duty: gotta pay for the “best”, also the “not my money” problem), likewise for large sources of funding (eg. pension funds) who are seduced by the upside promised (leading to high demand). Until they do, high margins will likely stay elevated.

Hope this drives the debate further so we can all get the full picture…

Figure 4.1: Real Corporate Profits, Financial vs. Nonfinancial Sectors strikes me as tracing the lifecycle of a bubble.

Compare it with Dr. Rodrigue’s Bubbles and Mania Chart.

The early ’80s dip is a Bear Trap, whilst the financial crisis would be a pretty severe Bull Trap. Assuming that we’re following that script then we’re in the Return to Normal phase prior to another plunge.

I don’t have anything material to add, but I want to comment on the unusually high level of discourse in this comment section. It is a testament to the thoughtfulness of Mike and his readers.

I strongly question calling the policies “deregulation” or “free market” as they clearly involve massive government subsidies to a few politically well connected banks.

I think opponents of these policies need stronger arguments and more effective organization, drawing together the broad spectrum of Americans and indeed world citizens who are adversely effected by these policies.

To do this:

1. The enormous cost of these policies must be demonstrated and emphasized in simple and clear terms. The problem needs to be phrased in terms of people’s pocketbooks, their take home pay, their savings and retirement funds, and the profits of the many small and medium sized businesses suffering from these policies. For example,

http://www.cepr.net/index.php/publications/reports/too-big-to-fail-subsidy/

2. The use of terms like “investment”, “growth”, “innovation”, and “research and development” to promote and defend these policies needs to be aggressively confronted and debunked. It needs to be made clear that the trillions of dollars spent on housing in the 00’s and goofy telecom and Internet schemes in the 90’s represents trillions of dollars not spent on critical human needs such as energy production, more efficient energy systems, transportation, and so forth. We see the consequences of this in rising energy prices and a declining standard of living. Yet another bubble, whether involving investments in China or blinking gadgets here at home, would represent further disastrous diversion of trillions of dollars from productive activities.

3. The framing of the problem as one of “deregulation” versus “regulation”, the “free market” versus the “government” needs to be rebutted and avoided. Quite clearly, these are policies of huge government subsidies to a few giant politically connected banks. The fact that these banks have stockholders and the executives are not civil servants (they are in fact paid far more than civil servants and subject to less strict rules) does not mean they are not intimately connected with the government. It is certainly true the policies have been and continue to be promoted with labels such as “free market”, “deregulation”, “private sector” and so forth, but the reality is otherwise. Many businesses and people outside of a small and shrinking charmed circle are suffering from these policies, but are misled by the “free market” rhetoric. The implicit and explicit claims by the banks to represent the “free market” or “private sector” should be aggressively challenged and debunked; they are almost laughably absurd at this point.

4. The long standing tactic of blaming the failure of policies labeled as “free market” and similar terms (emphasis on labeled), with the failure then used to promote further policies labeled as “free market” or “deregulation”, on the government should be recognized and aggressively countered. Blaming the government for fiascos that follow policies labeled as “free market” is not unusual. It happened after the Savings and Loan fiasco of the 1980’s, the Internet bubble, the Great Depression, the California electricity market “deregulation” fiasco of 2000, and a number of other cases. Rather, this long history of “crying wolf” should be pointed out simply and clearly, that the purported “free market” policies are frequently selective deregulation combined with increases in government subsidies for politically connected firms, and once again that the aggresive use of labels such as “free market” does not mean the policy actually is “free market”. Certainly not in the case of the current Too Big to Fail policies nor the sharp increase in FSLIC guarantees during the Savings and Loan “deregulation” of the 1980’s.

Drawing a clear distinction between the present policies fraudulently promoted as “free market” or “deregulation” and actual “free market” or “deregulation” policies will enable opponents of these policies to reach out to private citizens, businesses, and organization across the political spectrum, all of whom are suffering greatly from these policies.

Sincerely,

John

Another aspect I’ve seen as an ‘underlying factor’ is that all the investment banks went public and suddenly the banks future was separable from the executives and traders futures.

To oversimplify, the change from boring banking to proto-crisis banking involved industry consolidation with boring banks with small territories that they owned marketwise, getting gobbled up by big banks, and then used those banks the way feudal lords use serfs. The branch bankers ceased to be the business model and became the funding source.

This empowered big banks to do big deals without the mess of a consotium of participants and he concomittant need to share profits with investment bankers.

I read the letter you co-signed, published on Huffington Post, to the Senate Leadership. I applaud you for signing the letter. In addition to your and the other signatories, I want to start a citizens campaign with the same or better letter. I hope you will post your letter on your blog and help others get involved.

Without massive voter intervention, the existing weak legislation will likely become even weaker. And we all know the what the result of that circumstance would be.

Thank you.

Pingback: Pesos, Ponzi, And Financial Sector Profits - Paul Krugman Blog - NYTimes.com

Pingback: Crotty claims profits high due to increased risk taking « UMass Econ in the News