“I had another comment I was going to make. You won’t be able to resolve it for me but I’ll raise it anyway. It strikes me that when one looks at the banking system, never before in our lifetime has the industry been under so much competitive pressure with declining market share in many areas and a feeling of intense strain, yet at the same time, the industry never has been so profitable with so much apparent strength. How do I reconcile those two observations?” (Paul Volcker, 1997)

Lots of interesting follow-up to Tyler Cowen’s article on financial regulation and inequality. Kevin Drum, Arnold Kling, Falkenblog, Tyler Cowen, and others.

I’d recommending splitting the argument into three questions: (1) Why is the financial sector so big? (2) Why is the financial sector so profitable? and (3) Why is the financial sector so risky? By emphasizing being “short on volatility” Cowen is able to loop the three together, but I think it is also worthwhile to dissect them.

A few points.

– As far as I remember, The financialization of the American economy by Greta R. Krippner argued convincingly that the increase in the financial share of the economy isn’t the result of the modern corporation splitting off internal financial work. The actual sector has grown. This is probably common sense, but it’s good to document.

– Being short on volatility isn’t sufficient for these problems, and may not even be necessary. Here’s the VIX index on the S&P 500. We can be short it, but it is unlikely that we’ll end up in the top 0.01% of the income distribution because it is competitively priced. We should watch for why counterparties can’t discipline these contracts. Cowen and Kling emphasize a time-inconsistency problem, where we can take out a big position that is profitable in the short run but not in the long run. The logical end-result of that is a Producer’s-style capital markets, where things are created to fail, like the Magnetar trade.

But we couldn’t put that off because our likely counterparty would demand capital if the position got away from what I posted. We could end up with contracts that are too volatile for our counterparty to watch us that way (jump-to-default risk), which is largely what happened and a major problem for clearinghouses to manage.

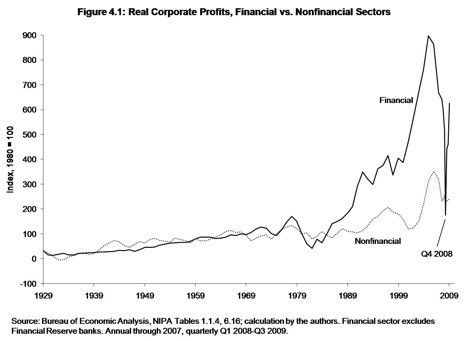

– The quote at the top is from this paper by James Crotty, which finds “If Financial Market Competition is so Intense, Why are Financial Firm Profits so High?”, which finds the reasons “are: rapid growth in the demand for financial products and services in the past quarter century; rising concentration in most major financial industries that makes what Schumpeter called “corespective” competition and the exercise of market power possible (thus raising the possibility that competition is not universally as intense as Volcker assumed); increased risk-taking among all the major financial market actors that has raised average profit rates; and rapid financial innovation in over-the-counter derivatives that allows giant banks to create and trade complex products with high profit margins.”

– Lehman didn’t get in trouble because it had too much leverage, it got in trouble because it’s liabilities were half on the order of one week and they had increasing haircuts. So leverage is one key, but thinking of leverage in two dimensions – how much and how “sticky” it is, how not subject to panic it is – is another. As Wallace Turbeville wrote “Bank runs by depositors have become a thing of the past because of the FDIC. The problem is not that the deposits are callable loans. It is that the derivative-embedded credit between banks and industrial companies are actually complexes of callable loans. Bank customers withdraw deposited funds when they become insecure. With trading, counterparties demand collateralization of all out-of-the-money risk when insecurity sets in. That’s what happened to Lehman and AIG, and Enron before them, as well as some lesser known institutions.

A bank run now happens at the trading level…Jimmy Stewart will no longer have to plead with his bank’s depositors. It will be someone like Jamie Dimon pleading with fellow bankers and corporate CEO’s.”

That chart kind of follows the growth of the internet. The digitization of financial data does allow for the opportunity to “double down” or simply create another offering by just changing some numbers.

” (1) Why is the financial sector so big? (2) Why is the financial sector so profitable? and (3) Why is the financial sector so risky?”

Good way to break it down. Another possible point are the distortions in the tax code (not just in the US), which can be a contributing factor to leverage and other problems. See IMF report to G20: http://www.imf.org/external/np/g20/pdf/062710b.pdf (starting page 61)

@Chris_Gaun

What they lack in profit, they make up for in volume.

Yes, it’s an old joke, but that doesn’t make it an untrue one. And note that the takeoff comes–not coincidentally, imnvho–when pensions go from Defined Benefit to Defined Contribution and when the IRA structure becomes default for “retirement savings.”

Large firms can negotiate with multiple banks. Individual “investors” who are adding $2,000 to $5,000 a year to an account–not so much.

If I buy US Treasuries at the auction average from my personal account, I do it through Treasury Direct and pay nothing. If I do it through an IRA, the charge is something between $25 and $45. Small amounts of free money add up.

And so the profits–in more ways than one–reflect present value gains from future retirement funds. The price of cat food better be going down.

I think that the first two questions can be answered with one easy explanation from Econ 101, that banking is a monopolistically competitive market, that larger banks have fewer competitors, and the large banks accrue outsize profits because of less competition. The third question is mostly about leverage.

Why is the financial sector so big? The easiest answer to that is that rewards in banking accrue to the largest banks. The larger the bank, the larger the loan you can make, the larger the IPO you can underwrite, etc. And the market for these large financial products is qualitatively different from the average financial product for the average consumer. Thus, banks get larger and larger, because the larger and larger you are, the more profitable the business.

I think that this is by far the largest drivers of the first two questions. The third is some function of leverage and the increased risk that these increasingly large transactions carry.

Pingback: Yglesias The Economics of Ripoffs « Politics

It is axiomatic that the reason an activity becomes highly profitable is high demand (= money to be had) and low supply (= takers for that money). The latter half of this equation can be expressed in three letters – SEC. The more interesting question is the first part. All that money has to come from somewhere. “Trading” is a zero-sum game.

It may be that the services investment banks provide are so valuable to investors, investees, or both, that they are worth the price. In an IPO, for example, the banks’ peofit presumably comes from the actual value of the company being greater than the capitalization. The owners desire to cash out makes it worth his while to let the banks walk off with a lot of his value.

I suspect, however, that most of the money comes from passive investors, such as pension funds. There is a reason why the people responsible for, say, the State of Oregon pension fund’s investments are flown to Switzerland and wined and dined, on top of there grossly exorbitant salaries. Other People’s Money.

So, I think the full equation reads

SEC + OPM = $$$

Pingback: How did we get this finance industry? – Original Positions